THE market has gained about 40 per cent in a year and is trading at an all-time high with mid-caps and small caps gaining around 65 per cent and 90 per cent, respectively, mainly driven by change in the sentiment led by the formation of a government with a strong majority and a Prime Minister who is the most pro-growth pro-investment leader in the world with the credentials, will and capability to deliver. But, this also makes Modi the biggest risk for the market — if something happens to him or if he fails to deliver. Besides a stable government that holds the promise of reforms, the market is rising due to change in the environment led by small steps such as scrapping of the Planning Commission, removal of diesel subsidy, launch of Jan Dhan and Swachh Bharat programmes, faster decisions and making the bureaucracy work, to name just a few.

The Indian market is riding on a structural story of positive demographics, a cyclical recovery, ample global liquidity, low commodity prices, especially crude, return of risk appetite with a revival in US economy and spurt in FII investment that has so far touched Rs. 94,000 crore during this year. Domestic mutual funds are also witnessing sustained inflows that have propelled them to invest Rs. 25,000 crore so far this year.

According to Christopher Wood, Managing Director of CLSA Ltd, “India is the most attractive equity market in the world from a five-year perspective with the economy bottoming out and a rating upgrade being just around the corner.” Most of the major economies of the world are facing ‘3D’ problems of high debt, adverse demographics and deflation. If the investment cycle can be revived with a few reforms, India can be well poised to notch up a growth rate of 7 per cent plus and a Sensex may well get to 40,000. The country is best positioned to benefit from falling commodity prices as against Russia, Brazil, and South Africa who are at the receiving end.

Inflation is going down faster than expected, giving a good inflation growth matrix that may well prompt the Reserve Bank to go for rate cut earlier than expected. With the kind of global liquidity unleashed by central banks like that of China, Japan and Europe, a lot is likely to flow to India, putting at rest the concerns raised due to rate hikes to be announced by the US Federal Reserve sometime next year.

There have been concerns very recently with regard to the stretched valuations and corporate earnings getting more misses than hits. The fact that the last three bull markets never peaked below PE of 25 times, that too happening in the 3rd, 4th or 5th year, the market at forward PE of 16 is at a reasonable distance and we are just in the first year of a multi-year bull run. The best part is that this time there is no competition from other emerging markets. As against the previous bull run that simultaneously witnessed rising commodity prices, the prices are on a decline, giving us a further edge. Moreover, the aggregate margins of Indian companies are at an 18-year low due to persistently high inflation, currency depreciation, low capacity utilisation, delays or stuck projects and weak demand. All this is likely to change and the corporate sector may witness a profit growth of 10-20 per cent as the margins move towards normal.

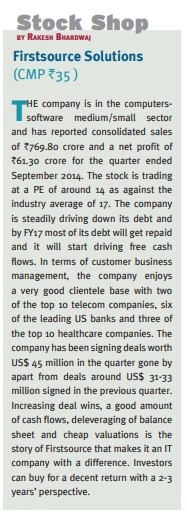

Investors are advised to invest with a long-term perspective and remain invested for a period of at least three years to reap decent returns. They should use any sharp correction to add good stocks to their portfolio.

The author has no exposure in the stock recommended in this column. gfiles does not accept responsibility for investment decisions by readers of this column. Investment-related queries may be sent to editor@gfilesindia.com with Bhardwaj’s name in the subject line.

{kind=link}