ANALYSTS are sharply divided over the sustainability of current recovery in the market that has witnessed the index recovering by around 6 per cent after falling 13 per cent to touch its lowest for the year during the second week of June. Those bullish about the market contend that most of the uncertainties, be it local or global, have either vanished or have been taken into account. A 23 per cent higher than average rainfall in the initial phase and kick-starting of the investment cycle by the government are the two strong points they cite on the local front. In the global context, it is believed that US Fed may not go in for a rate hike anytime soon, and when it does, the same is likely to be too modest and gradual to have a discernible adverse impact. Also, the Greece problem in all probability will either get resolved or the contagion may be too little to rattle the market. The current robustness of the economy has seen inflation going down significantly mainly due to softening of commodity prices. This has led to considerable improvement in the current and fiscal deficit scenario with forex reserves at $350 billion plus. GDP is further likely to pick up to around 8 per cent for FY 2016.

Those not so enthused by the current recovery say that El Nino will impact the remaining phases of rainfall in July-September. Also, the Lalit Modi expose is going to cast its shadow on the monsoon session of Parliament. Thus, no meaningful business will be carried out due to the opposition’s onslaught on the Narendra Modi government. The global scenario may also turn volatile due to Greece, the strengthening dollar and weakening Chinese economy. Corporate earnings are unlikely to pick up before the last quarter of the current fiscal and the huge NPAs of the banking system may soon cast its shadow. Excessive foreign debt in corporate balance sheets, most of which remains unhedged, is yet another cause of worry. Not happy with the scenario, FIIs have sold equities worth `15,000 crore during the past two months but domestic institutions bought stocks worth `26,700 crore. What has led to the recovery is the improved sentiment on the part of retail investors that made MFs collect around `90,000 crore during June 2014 to May 2015 – nearly double the previous peak in 2008.

The economy has albeit witnessed some green shoots that mainly include healthy growth in indirect tax collections in April-May that increased by 37.3 per cent y-o-y and were up 39.2 per cent in the first two months of the financial year. Central government spending witnessed a growth of 20 per cent and sale of medium and heavy commercial vehicles witnessed a growth of 24.66 per cent with car sales continuing their upward journey. The IIP was up 4.1 per cent compared to 2.8 per cent for the whole of the last financial year. The growth of the capital goods sector was most encouraging at 11.1 per cent. The HSBC Purchasing Managers Index (PMI) was at a four-month high of 52.6 in May.

Though the market may witness heightened volatility during July-August, it will offer an excellent buying opportunity. Investors may, therefore, gradually increase their exposure for decent returns over a period of two-three years.

The author has no exposure in the stock recommended in this column. gfiles does not accept responsibility for investment decisions by readers of this column. Investment-related queries may be sent to editor@gfilesindia.com with Bhardwaj’s name in the subject line.

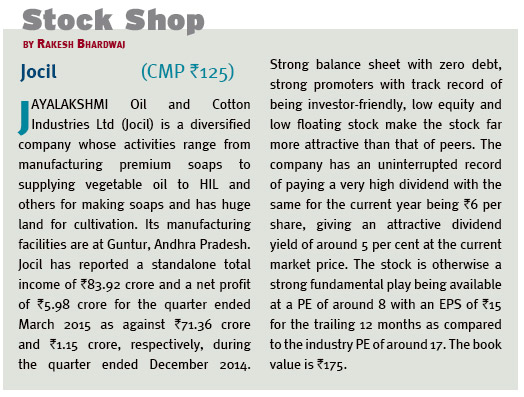

{kind=link}